Latest News

ECB Executive pens November 2025 rollout for digital Euro CBDC | MATIC News

The European Central Bank is pushing ahead with plans to launch a digital euro, aiming to provide a pan-European digital payment solution that complements cash, according to Piero Cipollone, Member of the Executive Board of the ECB. Speaking at the Convegno Innovative Payments conference, Cipollone outlined the fundamental design choices and rationale behind the digital euro project, according to notes released on March 13.

As evolving payment trends reflect people’s increasing preference for digital payments, the ECB seeks to make lives more accessible by offering a public digital means of payment that can be used free of charge for any digital transaction in the euro area. Cipollone emphasized that the digital euro would bring cash-like features to the digital world, being available offline, free for basic use, and respectful of privacy while having a pan-European reach.

However, some critics have raised concerns about the privacy implications of the digital euro. In a recent post, WalkerAmerica, the host of Bitcoin Bitcoin-focused Titcoin Podcast, expressed skepticism about the ECB’s claims of privacy:

“ECB plans to roll out digital Euro CBDC starting in 2025 They claim it’ll be ‘private,’ but it will not be, given Lagarde already wants to throw you in jail for a 1000+ euro anonymous cash payment. Study #Bitcoin & opt out of this totalitarian surveillance token.”

The released slides suggest the digital euro is designed to be accessible to everyone, including individuals and businesses, covering all retail payment scenarios in the euro area wherever digital payments are accepted. Cipollone highlighted the lack of a current European digital means of payment covering all euro area countries, with 13 out of 20 countries relying on international schemes for digital payments, settling 69% of all digital transactions in the EU. The digital euro aims to fill this gap by providing a standardized digital payment platform for the entire euro area.

Addressing inclusivity concerns, Cipollone noted that digital euro payments could also be made using a physical card, with cash being used for funding and defunding. Users would have access to face-to-face technical support and the option to switch intermediaries easily. Selected public entities would also serve as intermediaries for users without bank accounts.

Data protection and privacy are said to be key priorities for the digital euro project. The Eurosystem would implement safeguards to ensure high data protection standards, including internal data segregation and auditing. Innovative privacy-enhancing techniques would be adopted when ready and tested for large payment systems, fostering higher privacy standards for digital euro users.

However, the crypto industry has also been less optimistic about this, with people such as Bitcoin author Quinten Francois commenting that “Cash is anonymous and not censorable. Digital euro isn’t.” Further, in February, Cipollone spoke in front of the European Parliament’s Committee on Economic and Monetary Affairs to allay concerns about the security of the digital euro.

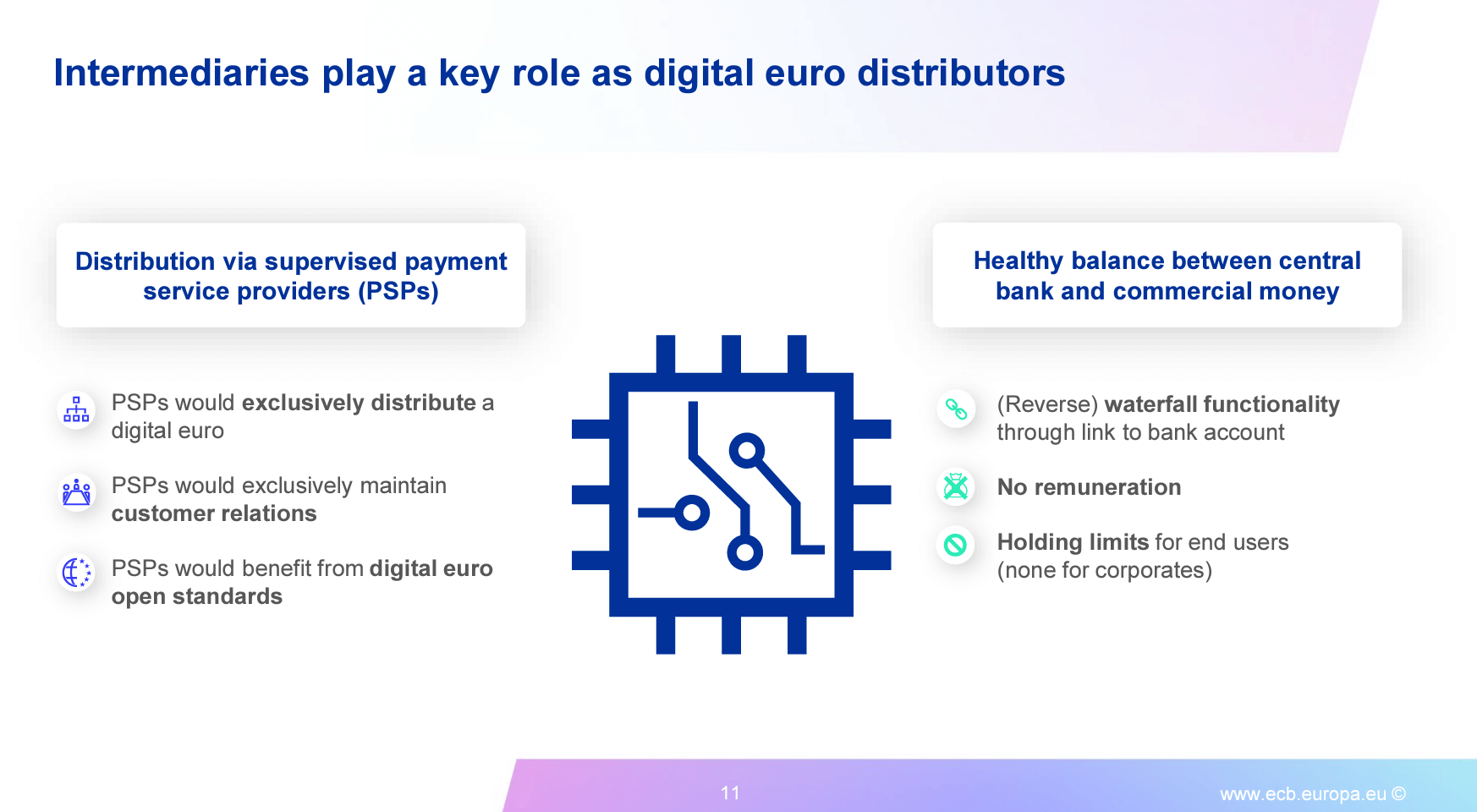

The presentation also asserts that the digital euro would be distributed via supervised payment service providers, maintaining a healthy balance between central bank and commercial money. PSPs would exclusively distribute the digital euro, strengthen customer relations, and benefit from open standards. A digital euro rulebook, drafted with the involvement of market participants, would establish common standards to ensure pan-European reach and a harmonized payment experience while giving the market freedom to develop innovative solutions.

Notably, the above slide showcases how there will be “holding limits” for end users. Still, there are none for “corporates,” suggesting that retail users will have a limit on how much of the digital euro they will be able to custody, but companies will have no limit. Such features aim to create a “healthy balance between central bank and commercial money,” according to the presentation.

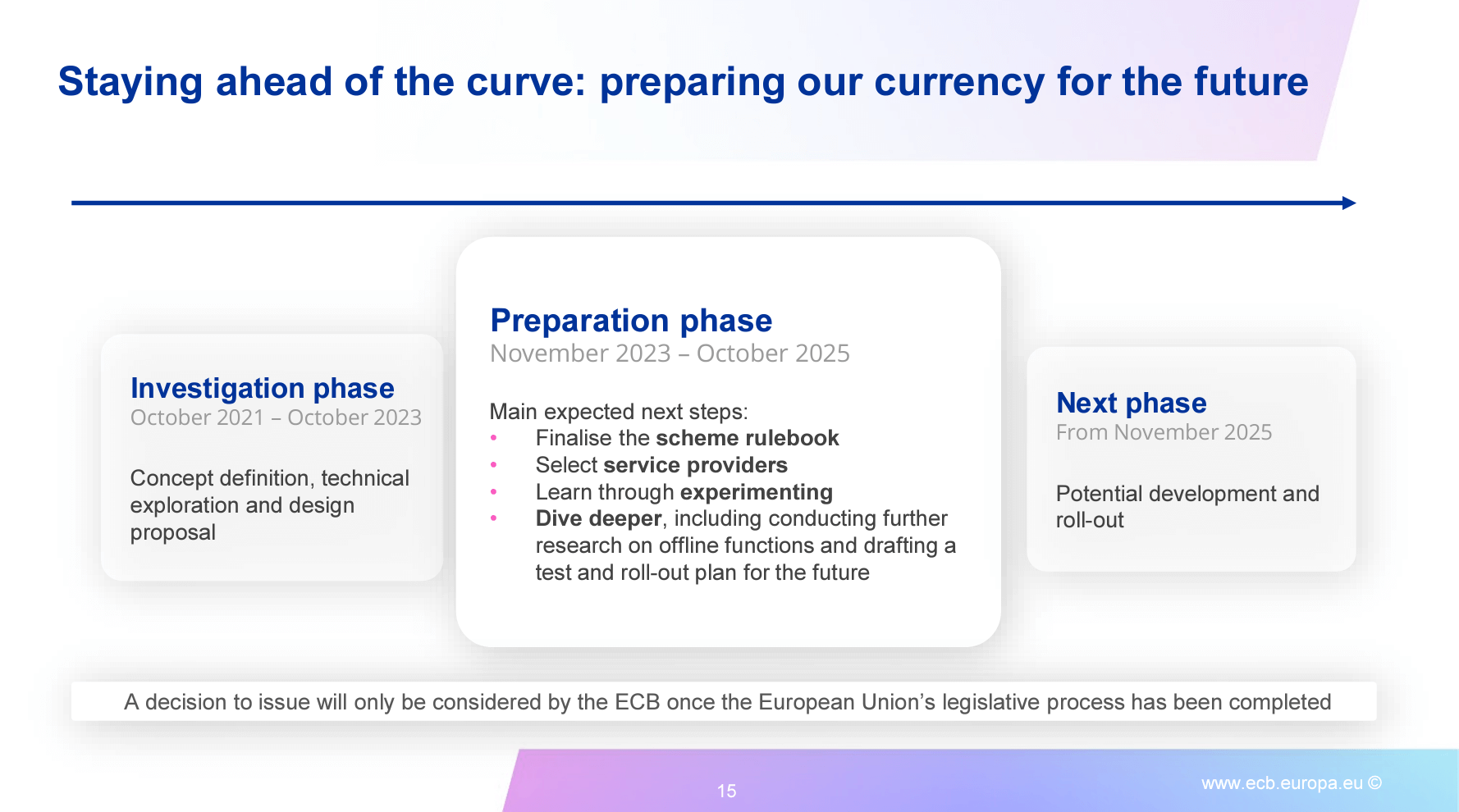

The digital euro project has passed its initial investigation phase (October 2021 – October 2023), focusing on concept definition, technical exploration, and design proposals. The current preparation phase (November 2023 – October 2025) involves finalizing the scheme rulebook, selecting service providers, learning through experimentation, and conducting further research on offline functions and test and rollout plans. A decision to issue the digital euro will only be considered by the ECB once the European Union’s legislative process has been completed. However, the document pens a potential rollout for November 2025.

As the ECB moves forward with its digital euro plans, the debate surrounding privacy and the potential for surveillance continues. Critics like WalkerAmerica urge individuals to study Bitcoin and opt out of what they perceive as a “totalitarian surveillance token.” The ECB will need to address these concerns and provide explicit assurances regarding data protection and user privacy to gain widespread acceptance of the digital euro.

The Bahamas will provide access to its central bank digital currency (CDBC) the “Sand Dollar” through commercial banks to increase adoption, Reuters reported on July 1, citing the country’s central bank governor.

Governor of the Central Bank of The Bahamas John Rolle said the country intends to establish the regulations within two years and has started signaling its intent to banks.

Rolle said:

“We foresee a process where all of the commercial banks will eventually be in that space and they will be required to provide their clients with access to the [CBDC].”

The Central Bank of the Bahamas reportedly sees the change as critical to raising CBDC and mobile payment adoption rates, even though banks will need to significantly modify their existing IT systems to comply with the upcoming obligations.

Rolle said uptake of the Sand Dollar is still limited years after its launch in 2020, requiring a shift from incentives to enforcement.

Adoption in question

Reuters described low adoption statistics amid the news. It reported that the CBDC accounts for under 1% of the country’s currency in circulation.

Reuters said wallet top-ups fell to $12 million in the eight months before August 2023 from $49.8 million in the same period in 2022, based on central bank data.

Rolle previously described “wide use, but very low average transaction value” in an interview with The New Times on June 19. He said 120,000 mobile wallets exist, equal to 20% of retail bank accounts, but mobile wallets make up less than 1% of retail payments.

Strong short-term data

A central bank press release from February described stronger short-term data. It recognized “modest seasonal growth in digital payments activities,” including the Sand Dollar, even though lower government transfer payments impacted overall year-to-date trends.

The bank said that the person-to-business (P2B) and business-to-business (B2B) transactions reached a combined $4.5 million, mainly involving the Sand Dollars, doubling from November 2022. It said personal wallet counts rose 20% year-to-date in December 2023. Sand Dollars in circulation rose 60.8% to $1.7 million.

Bahamas’ mandatory adoption policies could precede other strategies elsewhere. Reuters noted that the European Central Bank similarly intends to require retail and banks to accept and offer any future digital euro if it proceeds with one.

Latest News

Polkadot treasury holds $245M but faces revenue decline and two-year runway | MATIC News

The Polkadot Treasury holds assets equivalent to 38 million DOT, worth approximately $245 million. Head Ambassador Tommi Enenkel, popularly known as Alice and Bob, shared a new report providing the latest update on the network’s treasury.

This balance equates to about two years of the runway at its current spending rate. The report stated:

“At the current rate of spending, the Treasury has about two years of runway left, although the volatile nature of crypto-denominated treasuries makes it hard to predict with confidence.”

Polkadot’s first six months of spending

During the first six months of this year, Polkadot invested heavily in its ecosystem, spending 11 million DOT, valued at around $87 million, across various projects.

According to the report, the network invested about $37 million in Outreach activities such as advertisements, sponsorships, and events. The network signed sponsorship deals with race car driver Conor Daly and also pushed several marketing activities designed to bolster the network’s adoption by the broader global community.

Polkadot also spent $23 million developing its network features and upgrades, including SDK, Data Services and Indexing, Governance, and Subwallets.

Moreover, the network invested $15 million in liquidity incentives and $5.5 million in Talent and Education. Additionally, it spent $3.8 million to maintain the network and core ecosystem components, and another $2.1 million went towards Research.

Revenue decline

The report highlighted a decline in Polkadot’s revenue. During the first six months of the year, the network’s total earnings dropped to 171,696 DOT from 414,291 DOT, recorded in the second half of 2023.

Enenkel attributed this decline to the significant drop in network fees, which fell from 313,443 DOT last year to 39,444 DOT in the 2024 first half:

“We see that direct revenue from fees is still marginal. Polkadot made 300k DOT from fees in 2023-H2 from a short-lived inscriptions campaign. Fees under regular conditions are pretty stable with about 20k DOT per quarter. Other sources of revenue are typically transfers from accounts that return funds that they received and pay them back for various reasons.”

Disclaimer: CryptoSlate has received a grant from the Polkadot Foundation to produce content about the Polkadot ecosystem. While the Foundation supports our coverage, we maintain full editorial independence and control over the content we publish.

Latest News

Vitalik Buterin suggests ways to speed up Ethereum transaction confirmations | MATIC News

Ethereum co-founder Vitalik Buterin has suggested ways to help the blockchain improve its transaction confirmation times.

Buterin, in a June 30 blog post, explained that Ethereum’s Gasper consensus mechanism uses a slot-and-epoch architecture that contains certain complexities, like bug interactions and a 12.8-minute confirmation time, that makes it “more and more uncomfortable” for user experiences.

So, he highlighted some of the “practical options” Ethereum has to improve its user experience further.

SSF

Buterin stated that the single-slot finality (SSF) mechanism is similar to the Tendermint consensus, as it allows the finalization of blocks as soon as they are produced.

However, unlike the Tendermint consensus, Ethereum will keep the “inactivity leak” mechanism to allow chains to remain functional even if a third of the validators go offline. Buterin added that the single-slot finality mechanism also has its faults. Notably, all Ethereum stakers must publish two messages every 12 seconds, overloading the chain.

Meanwhile, Buterin furthered that while there are ideas to mitigate this issue, users may still have to wait 5-20 seconds. He wrote:

“There are clever ideas for how to mitigate this, including the very recent Orbit SSF proposal. But even still, while this improves UX significantly by making ‘finality’ come faster, it doesn’t change the fact that users need to wait 5-20 seconds.”

Rollup preconfirmations

Rollup preconfirmations aim to improve Ethereum’s Layer 2 (L2) solutions. These solutions process transactions with the same security as the Ethereum base layer (L1) but on a larger scale.

Rollups confirm transactions much faster than the current 5-20 seconds, targeting latencies of hundreds of milliseconds. This method divides responsibilities — the L1 network remains stable, censorship-resistant, and reliable, while the L2s offer faster transaction times and address user needs directly.

To achieve faster confirmations, L2s create decentralized sequencing networks. These networks have smaller groups of validators who quickly sign off on blocks, often within milliseconds, and commit them to the blockchain.

However, validators must ensure their commitments are consistent and trustworthy. If a validator signs conflicting blocks, they risk losing their deposits.

Based preconfirmations

Based preconfirmations leverage Ethereum proposers’ advanced capabilities, driven by Maximum Extractable Value (MEV) prospects.

The concept involves establishing a standardized protocol where users can pay an extra fee for immediate assurance that their transaction will be included in the upcoming block. This service, known as preconfirmations-as-a-service, would assure users of swift transaction confirmation.

Proposers who fail to fulfill their commitment or breach the agreement face penalties (slashing). Buterin noted that this framework will apply to L1 transactions and extend to L2 solutions. By treating all L2 blocks as L1 transactions, the preconfirmation mechanism ensures accelerated confirmations throughout the Ethereum network.

Buterin noted that Ethereum implementing SSF and rollup or based preconfirmations could significantly reduce transaction confirmation times.

However, he pointed out that this would return to the initial “epoch-and-slot architecture” the blockchain was trying to ditch. He stated:

“There is a deep philosophical reason why epoch-and-slot architectures seem to be so hard to avoid: it inherently takes less time to come to approximate agreement on something, than to come to maximally-hardened ‘economic finality’ agreement on it.”

He suggested that the network developers explore other options that are not as tightly interwoven as Gasper.

Mentioned in this article

Market Analysts Eye July for Potential Big Wins in Bitcoin and Ethereum — Here’s Why | MATIC News

Bahamas to provide CBDC access via commercial banks | MATIC News

Solana Trader Makes 307x Profit But Investors Raise The Alarm | MATIC News

-

Hot Projects4 months ago

Hot Projects4 months agoBitcoin Blasts Past $70,000 to Register New All-Time High | MATIC News

-

Latest News4 months ago

Latest News4 months agoCourt upholds SEC’s unregistered securities claims against Gemini, Genesis’ Earn program | MATIC News

-

Latest News2 months ago

Latest News2 months agoSix Coinbase customers claim the exchange is violating securities laws in new lawsuit | MATIC News

-

Hot Projects2 months ago

Bitcoin Will Be Set For New ATHs If It Breaks This Resistance: Analyst | MATIC News

-

Hot Projects3 months ago

Hot Projects3 months agoBitcoin ETF Inflows Could Eclipse $1 Trillion, Predicts Bitwise CIO | MATIC News

-

Hot Projects3 months ago

Hot Projects3 months agoOndo Finance Joins BlackRock Tokenized Fund As Inflows Surpass $160M | MATIC News

-

Latest News4 months ago

Latest News4 months agoOver $1 billion wiped off HEX’s valuation following Richard Heart’s disparaging remarks | MATIC News

-

Latest News4 months ago

Latest News4 months agoCathie Wood sees Bitcoin at $1 million sooner than 2030 after record ETF performance | MATIC News